Bottlenecks and variants slow down global recovery - Santander

Bottlenecks and variants slow down global recovery

Editor’s note: This article highlights insight from Santander’s Quarterly Market Outlook. While supply chain bottlenecks and SARS-CoV-2 (COVID-19) variants are having an impact in lowering short-term economic growth, pent-up demand and favorable financial conditions continue to support the path to full recovery.

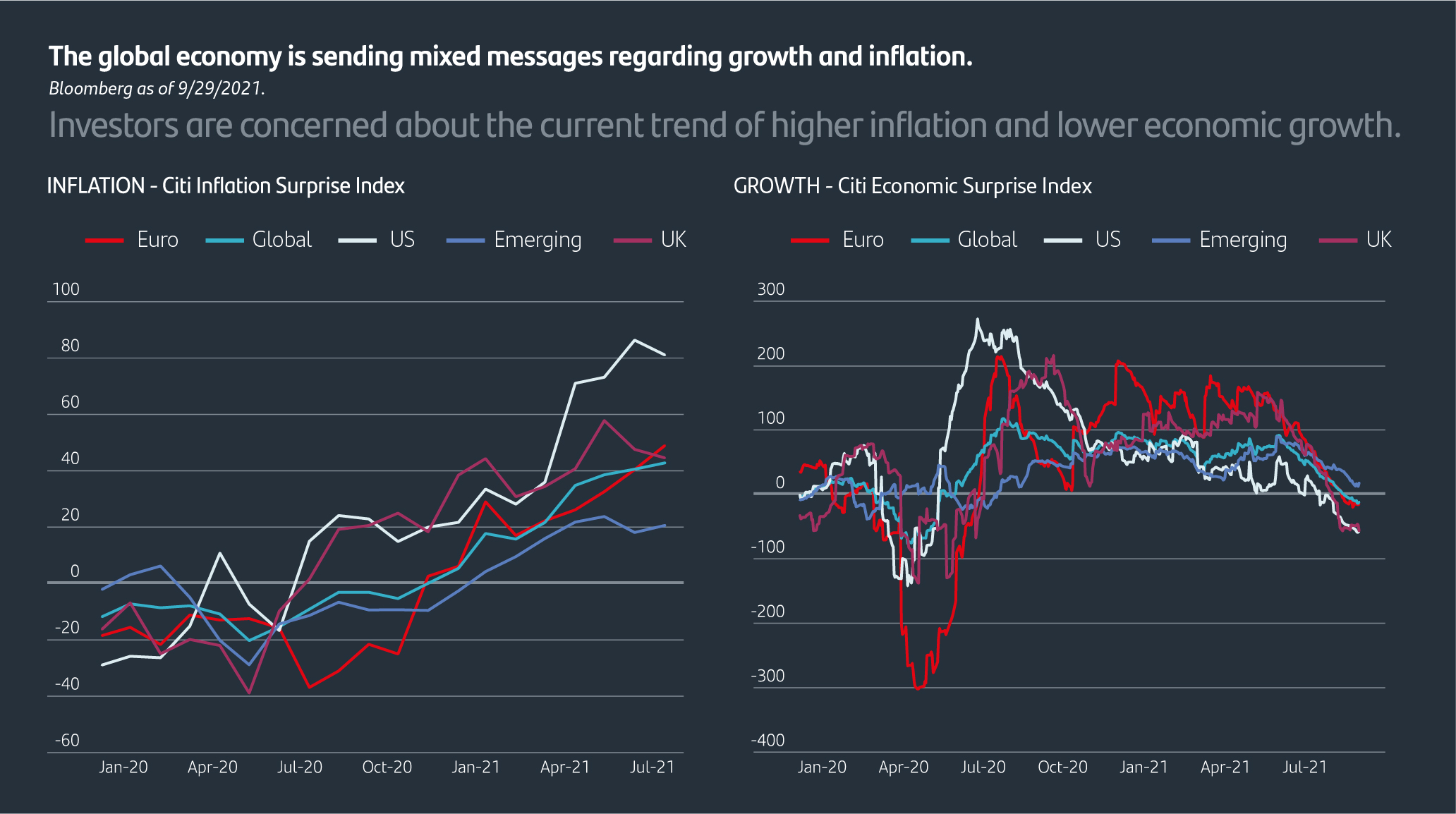

Mixed messages on the economic radar.

Investors are caught in the crosscurrents of inconsistent economic data and contradictory trends. Global difficulties in bringing COVID-19 cases under control is changing business expectations of a rapid economic revival, forcing companies to reset plans and revise forecasts.

Over the summer, expectations moved from a full reopening, triggering a strong and sustained recovery, to what now appears to be a slower and uneven one. The global consumer confidence index published by the Organization for Economic Co-operation and Development (OECD) continues to improve on a global basis, but it has started to show moderation in China and the US, which were among the first to recover from the pandemic. The rapid spread of the Delta variant seems to be the source of this recent loss of economic momentum, as the latest surge in cases coincide with the beginning of the decline in confidence.

Still, average household finances remain in good shape thanks to generous government stimulus programs in developed economies, and global financial conditions are very favorable for companies to invest. Europe’s economy is a good example of the strong recovery from the coronavirus crisis. Growth in the Eurozone outpaced both the US and China in the second quarter of 2021, more than 70% of EU adults are fully vaccinated against COVID-19, investment is strong, and unemployment is declining. Nevertheless, European Central Bank (ECB) president Christine Lagarde sounded a cautious note in early September saying, “We are not out of the woods,” and highlighted several risks over the coming months, despite the ECB raising its growth forecasts for the third consecutive time this year.

In the two graphs below, we can see the mixed signals coming from the hard economic data. Measures of economic “surprise” in activity indicators (i.e., a comparison of official data with economists’ forecasts) started to deteriorate and turned negative during the summer. On the other hand, inflation data has been higher than forecasts globally. Bring all these together and the picture is one of increasing uncertainty about whether the global economic recovery will carry on at a rapid clip. Economists see downside risks to the global economy but still expect robust growth for the remainder of 2021.

Path to normal requires booster shots.

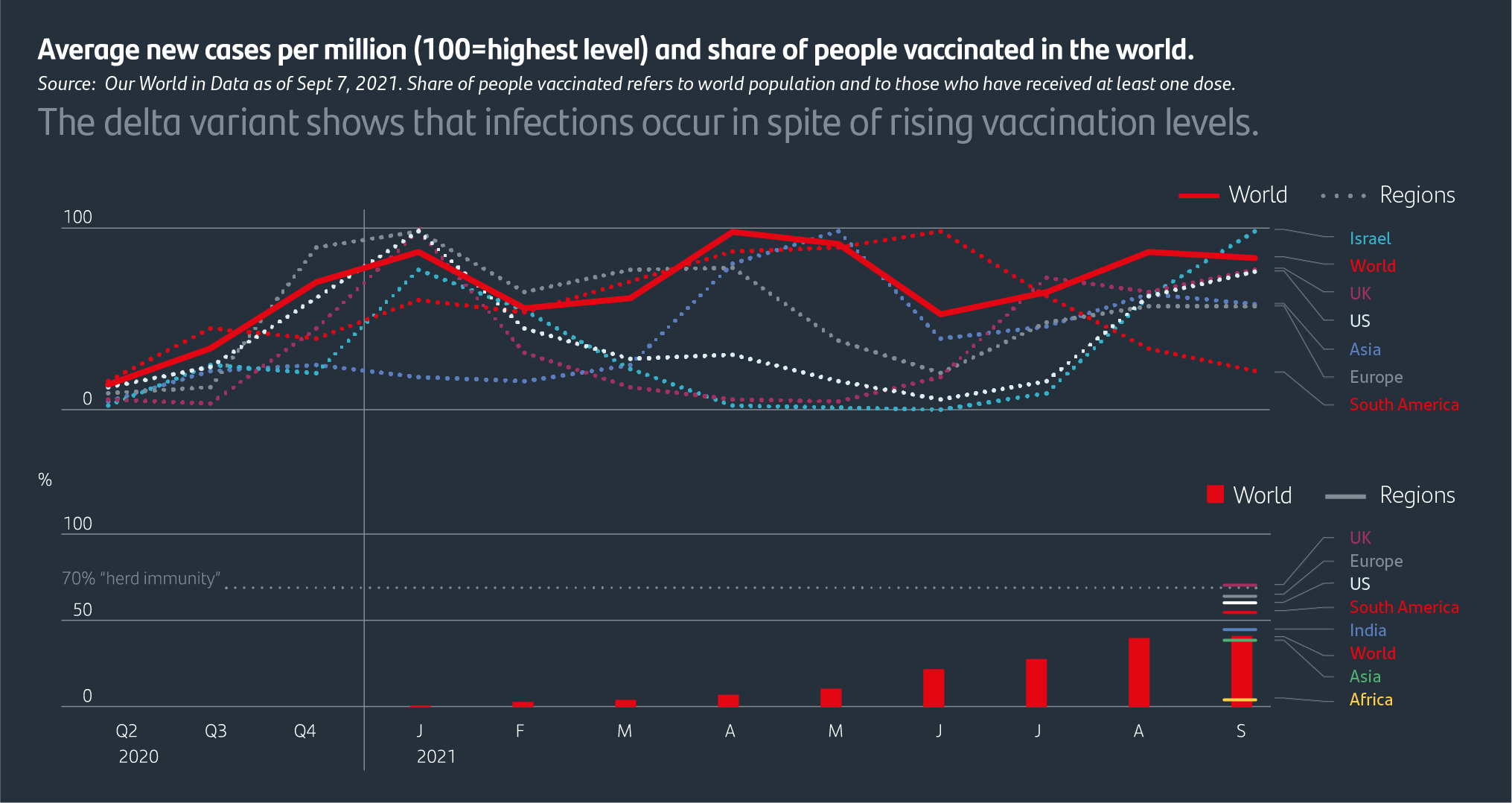

Almost 18 months have passed since the beginning of the pandemic, and the economy is gradually on the mend. It has strengthened as immunizations have increased. Still, the world is facing the Delta variant and the need for a booster shot seems to be the only way to maintain a high level of effectiveness.

By the end of 2020, it was estimated that herd immunity would be achieved with 70% of the population inoculated. According to Our World in Data, data as of September 7, 2021, which compiles all data available in the world regarding COVID-19, the share of population with at least one dose is over 40%, with the European Union at 65%, the United States at 62%, South America at 56%, Asia at 46% and Africa at 5.5%. The graph below shows that, while it is true that new infections generally declined around June, the emergence of the Delta variant was responsible for more than 90% of new infections in the United Kingdom and has led to new peaks of infections in most countries and regions, especially among the unvaccinated.

Faced with this spike in infections, countries have reacted in different ways. The United States and the United Kingdom tried to remain on the path of normalcy, while other governments such as China, Australia, New Zealand and most of Southeast Asia imposed tighter restrictions. Renewed lockdowns in Asia, a key producer of much needed intermediate goods, diminished economic activity and caused even more supply bottlenecks with two consequences: price increases and an economic slowdown elsewhere due to scarcity of those goods. As a result, the the Delta variant could be causing "stagflation," the combination of stagnant economic growth and high inflation.

“The possibility of new COVID-19 variants that bypass vaccines continues to pose the biggest risk to market stability and economic growth.”

Vaccine hesitancy will likely diminish as evidence of their effectiveness continues to mount. A UK analysis by Public Health England (PHE) as of June 2021 showed that two doses of the Pfizer- BioNTech vaccine was 96% effective against hospitalization from the Delta variant, while the Oxford-AstraZeneca vaccine was 92% effective. It has also been shown that the effectiveness of the vaccines decreases over time, so a booster dose could become necessary to maintain the path of economic normalcy. The higher the infection rates caused by the new variants, the higher the required vaccination rate. Nevertheless, we do not see this as a showstopper for the recovery as the players in the economy have become used to dealing with such uncertainties – authorities included. However, the possibility of new COVID-19 variants that bypass vaccines continues to pose the biggest risk to market stability and economic growth.

Bottlenecks are bad news for short-term growth and could lengthen the recovery.

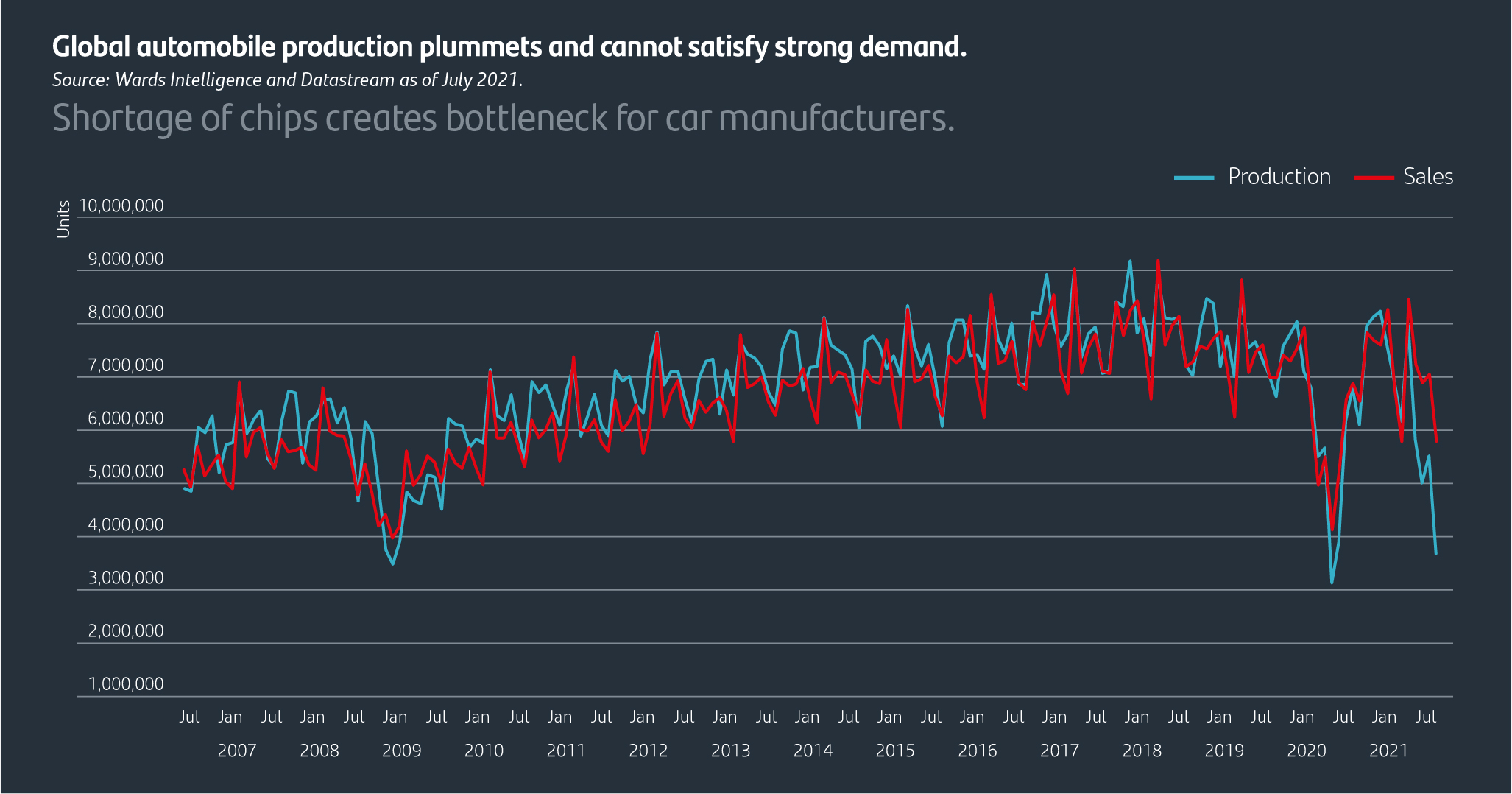

Supply chain disruption has been in the news. It is somewhat sensationalist because while some products have reduced supply, global manufacturing output is near an all-time high. The problem seems to be a supply-demand imbalance rather than a problem of “less supply”. The scarcities seem to go beyond the realm of anecdotes. We have to go back to the mid-1970s to find similar delays in supplier deliveries. Present business surveys conducted by IHS Markit indicate that manufacturers’ backlogs of work are increasing. We can see a clear example of the impact of shortages of semiconductors and staff in the automobile industry (see graph below) that was forced to cut production significantly to properly allocate the limited number of microchips to its automotive assembly plants.

Throughout 2021, consumers in developed economies spent the savings that they had accumulated during the lockdown periods. Much of that spending was on goods rather than services due to pandemic restrictions on the service sector, and because consumers feel safer avoiding service-related businesses. This led to an extraordinary level of demand for goods increasing spending on durable goods significantly above trend.

The boom is creating two kinds of bottlenecks. The first relates to supply chains. There are shortages of everything from timber to semiconductors. The second is in labor markets. In August, the United States created only 235,000 jobs, far fewer than the expected 720,000. Yet job vacancies are at all-time highs, and firms are struggling to fill positions.

Some of these bottlenecks should ease over the coming 12 months. Global supply chains will be adjusted and strengthened, and the labor market will adapt to new spending patterns. While recovery from the pandemic will be far from smooth, the good news is that there is still plenty of pent-up demand in many industries (housing, auto, semiconductors, etc.), therefore the economic recovery doesn't seem to be threatened by short-term shortages.

Economic cycle is past the peak of growth.

Economic momentum has slowed over the past few months. Confidence indicators reveal bifurcated economic performance among major developed markets as well as divergence with emerging markets. Rising infections, production bottlenecks, labor supply constraints and the end of several stimulus measures in the United States specifically, are prompting an economic slowdown although levels of growth are still very high— in most of the largest economies. Moreover, sky-high economic growth rates following the initial pandemic slump in economic activity were ultimately unsustainable after the sharp rebound from last year's deep downturn.

Negative pandemic dynamics continue to weigh on economic activity in Australia and Japan where infections are rising, and severe measures of lockdowns are being implemented. Services PMIs (Purchasing Managers Index) worldwide fell sharply, and manufacturing activity is also slowing.

The US and the UK are also experiencing waves of infections that are causing greater than expected manufacturing and services slowdown. Restrictions have not been tightened and infections seem to be on the rise, dampening consumer activity as well.

On the bright side, confidence indicators for both the services and the manufacturing sectors reveal the Eurozone is showing resilience. As we mentioned last quarter, economic recovery in this area was running behind the rest of the world which probably peaked in Q2 and now it is catching up.

Emerging economies were hit by the Delta variant at an early stage of economic recovery and are struggling with weak domestic conditions. China is no different than other large countries and is also experiencing economic moderation in the second half of the year.

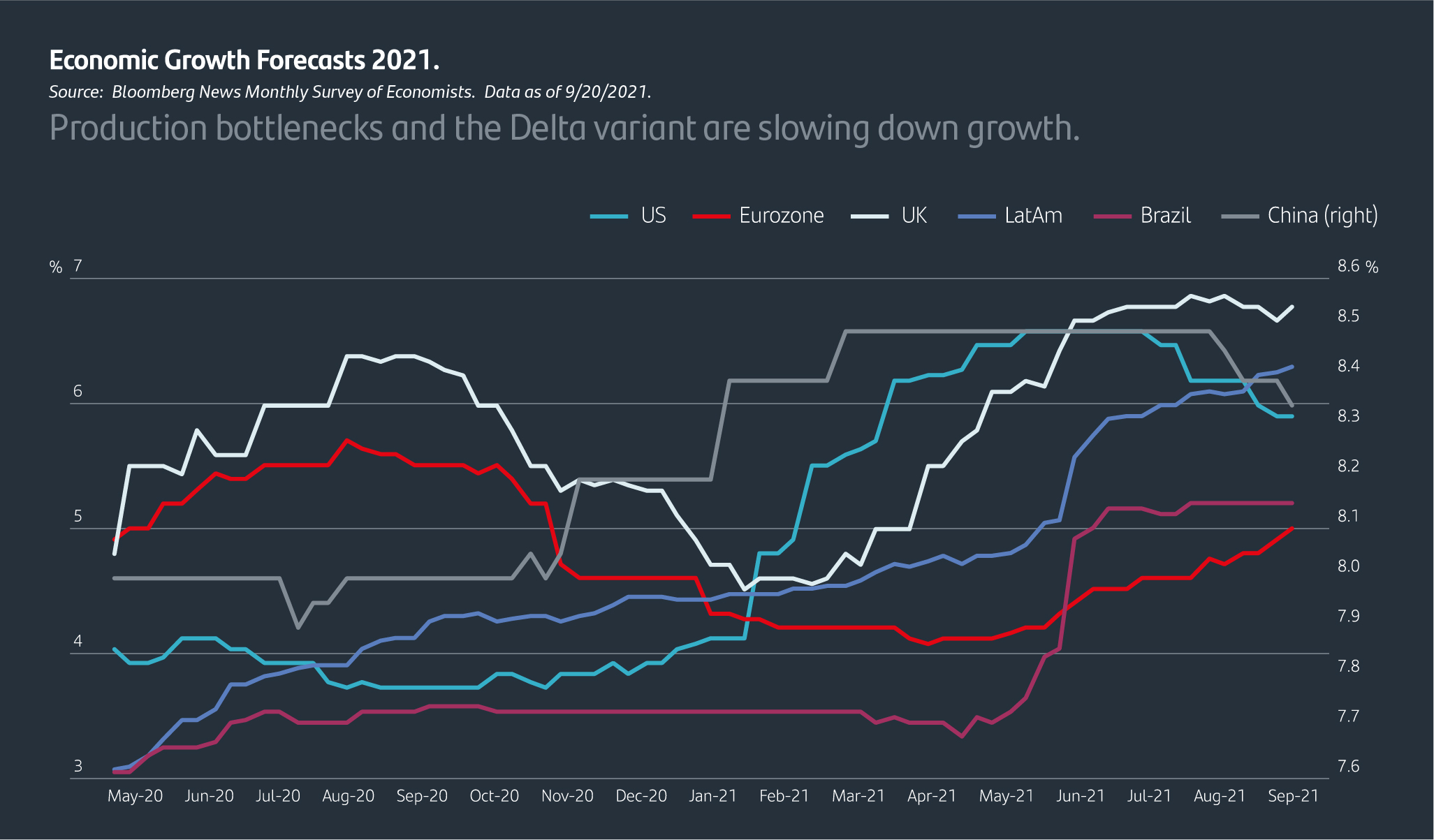

The above has already led to downward revisions to economic forecasts (see the graph below) in the largest economies over the past couple of months. As we mentioned, the Eurozone and Latin America are experiencing a lag in the recovery and downward revisions could come later in the year. Still, Bloomberg News Monthly Survey of economists as of 9/20/2021, estimates that global growth will be around 5.9% this year and 4.5% in 2022.

To learn more about market shifts and tap into expert advice, get access to customized financial plans and a financial consultant as a Santander Private client.

Securities and advisory services are offered through Santander Investment Services, a division of Santander Securities LLC. Santander Securities LLC is a registered broker-dealer, member FINRA and SIPC and a Registered Investment Adviser. Insurance is offered through Santander Securities LLC or its affiliates. Santander Investment Services is an affiliate of Santander Bank, N.A.

| INVESTMENT AND INSURANCE PRODUCTS ARE: | |||||

| NOT FDIC INSURED | NOT BANK GUARANTEED | MAY LOSE VALUE | |||

| NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | NOT A BANK DEPOSIT | ||||

![]() Santander Bank, N.A. is a Member FDIC and a wholly owned subsidiary of Banco Santander, S.A. © 2022 Santander Bank, N.A. All rights reserved. Santander, Santander Bank, the Flame Logo are trademarks of Banco Santander, S.A. or its subsidiaries in the United States or other countries. Mastercard is a registered trademark of Mastercard International, Inc. All other trademarks are the property of their respective owners.

Santander Bank, N.A. is a Member FDIC and a wholly owned subsidiary of Banco Santander, S.A. © 2022 Santander Bank, N.A. All rights reserved. Santander, Santander Bank, the Flame Logo are trademarks of Banco Santander, S.A. or its subsidiaries in the United States or other countries. Mastercard is a registered trademark of Mastercard International, Inc. All other trademarks are the property of their respective owners.

Personal Banking Investing Small Business Commercial Private Client

Privacy Policy | Terms of Use | Accessibility | © 2025 Santander Bank, N. A - ![]() Equal Housing Lender - Member FDIC

Equal Housing Lender - Member FDIC